The great amplifier

Appreciation happens when you add value to an asset. We learned all about that in the previous section.

Leverage amplifies gains and losses.

Let's talk about gains first.

The basic principle is that you realize appreciation not only on the cash you put into the deal (25%) but also the cash the bank put into the deal (75%).

On a property worth $1MM let's do some math here. Let's assume appreciation over time at 5% per year for the first 5 years of ownership.

That means the property appreciates by $50k the first year and then 5% every year thereafter.

Your equity over time:

The bank loaned you the money to buy the asset but they don’t realize any appreciation, you just need to pay them back with interest. BUT THE ENTIRE ASSET GROWS.

Even at a 2.5% inflation, this is what it looks like:

You’ve added over $150k to your $250k investment in 5 years.

Now an important note here:

This may work automatically for residential houses in growing cities, but remember that commercial real estate is valued based on NOI and not rising costs of living.

So how do we raise net operating income and make our property more valuable?

The answer is to raise revenue slowly over time to the point that it out-paces expenses. In self-storage, we raise rents on current tenants 6% every 9 months. We also see a 3-5% annual street rate increase (or more if we are in a market without much supply).

That, evened out, generally means we can grow revenue by 4-6% each and every year even after we are stabilized (already full of tenants).

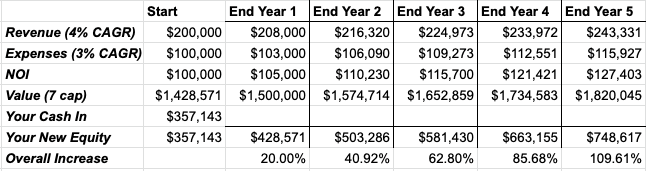

This is when we need to talk about CAGR.

“Compounding Annual Growth Rate”. How much is each lever in this massive equation changing in a given year?

If your expenses grow at 3% and you can increase your revenues at 4% per year, which we try to do in the self-storage business, this is what happens to the value of your equity in the asset over time:

Since your equity is only 25% of the overall pie, and the revenue is already 2x as large as the expenses / assuming a 50% expense ratio here (self-storage is even lower of an expense ratio and these levers are even more powerful), your equity more than doubles in a 5 year period.

This is not a value add deal, it is simply a fully stabilized property chugging along and letting father time work its sweet sweet magic.

And this, my friend, is why I never like to sell real estate. Because over the course of 5 years you can double your amount of equity in a deal just by tugging on a few levers and being a good operator.

But wait, there is more! (I feel like Billy Mays selling magic cleaner)

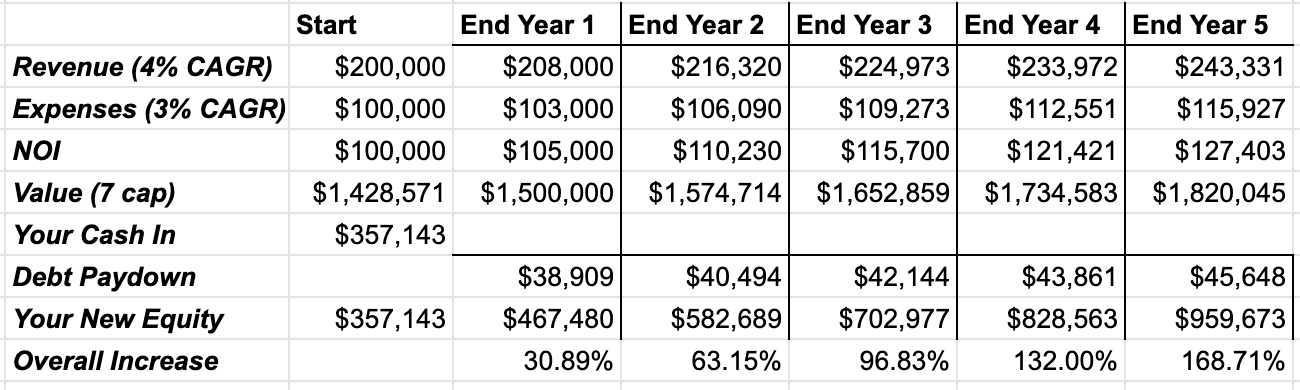

If we have a 25-year amortization schedule and a 4% interest rate we pay back some debt each year as well. The payment stays the same but you pay off MORE debt each year. The interest amount goes down and the principal amount goes up.

Run an amortization calculator on https://www.amortization-calc.com/mortgage-refinance-calculator/ and you’ll see the magic.

It is like a forced savings account. Yes, it sucks your cash flow, but you are slowly building more equity every single month.

In this example, with a 75% LTV loan at 4% on a 25 year am, we have added back the debt pay-down to your equity number, along with the 4% growth in revenue and 3% growth in expenses:

Your initial $357k in equity (your cash into this deal) has turned into $959k.

How about that for long-term wealth building?

And this isn’t even taking into account cash flow! Let's see how it looks when we model out our cash flow and get a feel for our overall position on this investment.

Powerful, powerful stuff.

So now what? Do we sell? Let's talk about our options in the next section.

Note: Leverage can amplify losses just as easily as it can amplify gains. We'll cover the risks in greater detail in the "risks" section.